The moment the monks began openly defying the military regime in Myanmar, there was always going to be only one outcome - violent suppression. The fact that blood was spilled should not come as a surprise to anybody save the most idealistic and naive. The logic is perfectly simple - dictators who lose power often lose everything, and sometimes even end up in tribunals. Any rational person faced with this set of odds would always resort to violence to save himself.

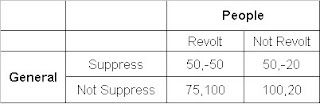

A Heuristic Game Matrix

The above is a simple game matrix. On the left, we have the General, who has two courses of actions (Suppress, Not Suppress). On the top, we have the People, who can choose to (Revolt, Not Revolt). The payoffs are given in the 2x2 matrix, the number on the left denotes the General's payoff while the number on the right denotes the People's payoff. The payoffs applied here are very simple. If the General does not suppress (and his People do not revolt), his payoff is 100. Every time the General suppresses, he pays a political price and his payoff drops to 50. However, if the People revolt and the General does not suppress, he loses everything and gets 0. Whenever the General suppresses, the People's payoff becomes negative (bloodshed).

Clearly, the best outcome for the People is that they revolt, the General not suppress, and the revolution succeeds. In that case, the People gets 100. But is this a rational outcome? No, it cannot be. Faced with the outcome of losing everything when the People revolt, the General surely will suppress. Bloodshed is inevitable.

Rewarding the General

Can we ever find a way out of this logical jam so that the People can be better off? Yes, it is indeed possible but only if we come down from our moral high horse. Consider the next matrix.

There is only one number that I changed - in the lower left box where the General's payoff is changed from 0 to 75 (it has to be larger than 50). Immediately, the lower left box of (Not Suppress, Revolt) becomes established as a Nash equilibrium. When the People revolt, the General will choose not to suppress and get the payoff of 75, which is greater than the 50 he will get if he suppresses.

Logical Response

What does this simple analysis tell us? Short of a military intervention to carry out regime change, no amount of outside pressure or condemnation can ever help the Myanmese people. Sure, outside condemnation hurts but only as far as reducing their payoffs for the generals. But faced with the prospect of losing every thing should the revolt succeed, the only logical response is for them to suppress. The greater the threat, the more brutal the suppression.

Instead, the only way out is for the world to reach a settlement with the junta that rewards the generals for non-suppression. This may sound morally odious to those who believe that the generals should be punished for their crimes. But by cutting off the exit for the generals, we are in fact condemning the Myanmese people to more bloodshed. Herein lies the big moral dilemma. Should we reward the perpetrators of violence?

Swallow our Moral Indignation

Are there any historical precedents? Plenty. South Africa comes to mind first and foremost. Former white regime members were not tried for their crimes against the black people, there was merely the Truth and Reconciliation Tribunal where the whites were asked to confess their wrongdoings. Pinochet in Chile was made Senator-for-Life and continued controlling the armed forces even though the civilians were supposed to be in charge. Nearer to home, we have Marcos. As he was a key US ally during the Cold War, the US provided a safe haven for Marcos and his family to take their billions and comfortably retired to Hawaii.

Swallow our moral indignation, provide a safe haven for the generals with state protection, let them keep their billions, and guarantee that they never have to face any tribunals. To help the Myanmese people, we must consider rewarding the generals even if it is morally and politically difficult for us to do so.

posted by Bart JP at

8:12 pm

|

29 comments

![]()